OECD is updating the rules on intra-group services — what the draft covers.

On 1 June 2026, the OECD published a public consultation document proposing revisions to Chapter VII of the Transfer Pricing Guidelines — the chapter governing intra-group services, one of the most common transaction types within multinational groups. Comments are open until 22 July 2026, and a public consultation hearing is planned for November 2026 in Paris.

The revisions do not change the underlying principles. Instead, they align Chapter VII with the delineation framework of Chapters I–III, clarify long-standing grey areas, and — for the first time — provide 21 worked examples.

In brief

The OECD has proposed a revised Chapter VII of the Transfer Pricing Guidelines, covering intra-group services — comments are open until 22 July 2026.

The benefit test is clarified and kept strictly separate from arm's length pricing; shareholder activities remain non-chargeable.

No transfer pricing method is treated as the default — including cost-plus.

The 5% simplified mark-up for low value-adding services is retained, but with a tightened definition of qualifying services.

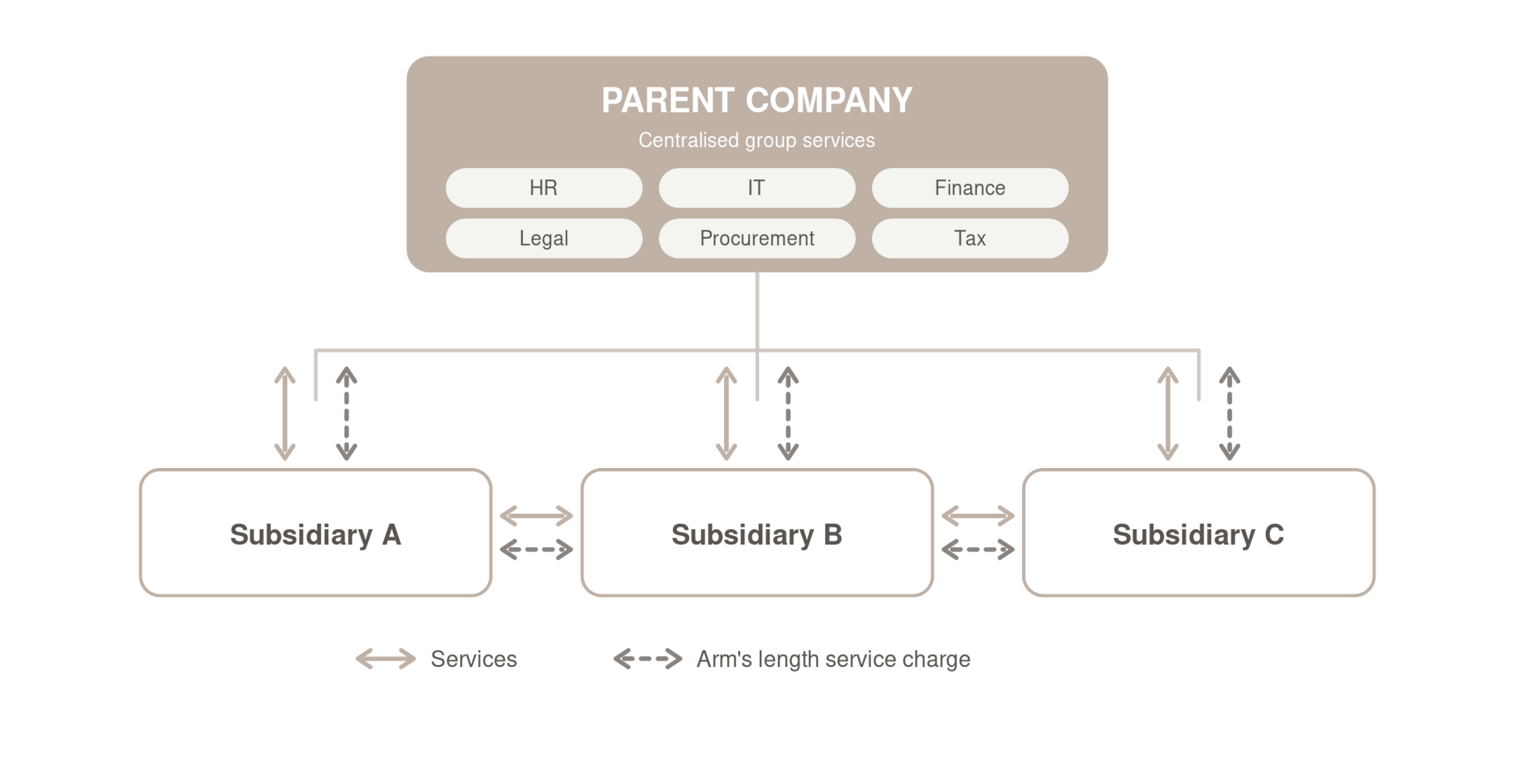

Intra-group services diagram

Accurate delineation comes first

The analysis must start with identifying the actual transaction. Labels and written contracts alone do not determine whether a service has been rendered — economic substance governs.

The benefit test is clarified

An activity qualifies as an intra-group service only if it provides economic or commercial value that an independent enterprise would have been willing to pay for. The draft clarifies that the benefit must be reasonably anticipated at the time the activity is performed — not guaranteed — and that the benefit test and arm’s length pricing are separate analyses that must not be conflated.

Shareholder activities are not chargeable

Activities performed solely because of ownership interest — consolidation of accounts, stock exchange compliance, investor relations, parent-level tax compliance — are shareholder activities and cannot be charged to subsidiaries. The draft also clarifies the boundary: a parent’s actions are not automatically shareholder activities merely because senior management performs them.

Duplication and incidental benefits

No charge is justified where a service fully duplicates one already obtained from another party, or where benefits are indirect and remote. On-call services may constitute a standalone service even if not actively used — usage data over multiple years can inform the analysis.

No default transfer pricing method

The draft explicitly states that no single method — including cost-based methods — should be assumed as the default. CUP applies where comparable uncontrolled prices exist; cost-plus and TNMM remain widely applicable but require careful cost base construction, particularly regarding pass-through costs; profit split is appropriate in highly integrated arrangements.

Documentation expectations rise

Beyond the Master File and Local File, the draft recommends contemporaneous evidence: descriptions of expected benefits, communications related to scope decisions, technical documentation, and output delivered. For indirect charging, documentation should cover the cost pool calculation, allocation key rationale, and the split between pass-through and marked-up costs.

Low value-adding services: 5% retained, scope tightened

The simplified approach with a 5% mark-up is retained, but the definition of qualifying services is tightened. Manufacturing, sales, R&D, financial transactions and group management are explicitly excluded — and the 5% safe harbour must not be used as a benchmark for services that do not qualify.

What this means in practice

The draft strengthens the case for robust contemporaneous documentation and moves away from assumption-based cost-plus pricing. Groups relying on broad low value-adding treatment should verify their services genuinely qualify under the tightened definition. Service charging structures and documentation are worth reviewing before the guidance is finalised.

How does this affect your group?

A short introductory call is always free — book a call.

The full consultation document is available on the OECD website.